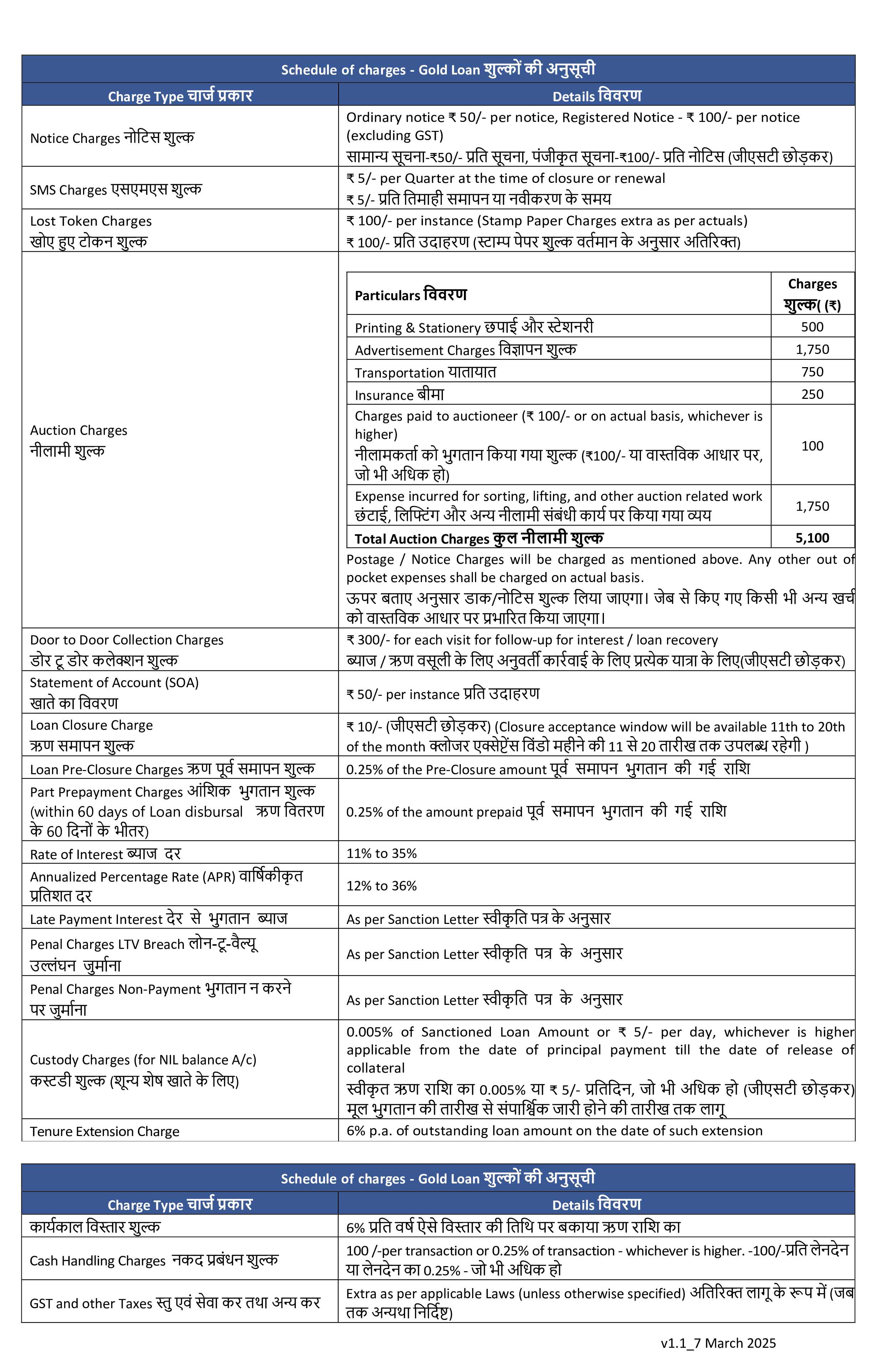

In times when financial flexibility is paramount, SMC Finance brings you a hassle-free and swift solution to meet your immediate cash needs. Our gold loan product is designed to empower you with quick access to funds while leveraging the security of your valuable gold assets.

Here is an example, to calculate the total cost of your SMC Gold Loan

Representative Example : If the gold loan amount is Rs 100,000 and the customer selects a scheme with interest rate of 15 % per annum and processing fees of Rs 100/- with one year tenure.

So, Total cost of the loan would be (Interest + Processing fee) = Rs 15,100.

APR (Annualized Percentage Rate) would be 15,100/100,000 = 15.10% p.a.

Minimum period of repayment is 6 months and Maximum period of repayment is 12 months.

Subject to the necessary KYC and verification. T&C apply

- 18ct-22ct of gold jewellery

- Bangles, Chain, Ear rings, Rings, necklace, etc.

- Jewellery shall be self owned

- No loan granted against gold coins, gold bullion, gold bars etc.

- only gold value will be considered (excluding Stone weight)

7th March 2025

- Aadhaar Card

- PAN Card (Mandatory if Loan Amount > ₹ 50,000)

- Nominee Details

- Mobile No. (will be validated using OTP)

- Customer has to be present in the branch

What is a gold loan?

A gold loan is a loan obtained after pledging gold jewellery as collateral to a gold loan bank. The loan amount is calculated on the basis of the quantity and purity of gold.

Can I release a part of my gold?

Yes, you can. Once you have paid the amount based on the value of the gold, you can partly release your gold.

Where can I repay my loan amount?

You can pay your SMC gold loan through the app , or through UPI payment or visit your branch to pay the amount in cash. As a regulatory requirement we cannot accept third party payments.

How much time does it take for loan approval and what is the gold loan interest rate?

Maximum processing time to disburse SMC Gold Loan is max. 30 mins. You can get the best attractive interest rate with SMC Gold Loan based on the Gold loan scheme suitable to your requirement.

How will the value of my gold be calculated?

The value of the gold is calculated in accordance with the per gram rate in the market. Therefore, the amount will be gold loan per gram of gold jewellery to be pledged with SMC Gold Loan. While evaluating the weight of the jewellery, only the gold parts are calculated and the stones and other metals are not considered.

What is the kind of security against which I can avail the loan?

You can avail the loan against the pledge of your household ornaments. The loan offered shall depend upon the purity level of your ornaments and the net weight of gold content.

Can I avail loan against my gold bullion (coins, gold bars, gold biscuits etc)?

As per regulatory guidelines, we are not permitted to finance against the pledge of your gold bullion, bars, biscuits, coins or raw gold. For more information on the type of ornaments that can be accepted as pledged for gold loan purposes please visit your nearest branch of SMC Gold Loan

How do I know that my gold is safe with you?

Our staff follows strict operating guidelines while handling customer ornaments. This avoids ornament breakage and loss. The ornaments are kept in safe custody (safe rooms or strong rooms) with adequate security measures in the branch. There is 24 X 7 surveillance of the branch with help of our security partners.

Is there any maximum and minimum limit for availing Gold Loan? What about the tenure of the loan, lock-in period?

SMC Gold loans can be availed for any amount between Rs. 5,000/- to a maximum of Rs. 25,00,000/-. Loans can be availed for a period of min 6 months to max 12 months. Our gold loans have a minimum lock period of 7 day.

In times when financial flexibility is paramount, SMC Finance brings you a hassle-free and swift solution to meet your immediate cash needs. Our gold loan product is designed to empower you with quick access to funds while leveraging the security of your valuable gold assets.

- 18ct-22ct of gold jewellery

- Bangles, Chain, Ear rings, Rings, necklace, etc.

- Jewellery shall be self owned

- No loan granted against gold coins, gold bullion, gold bars etc.

- only gold value will be considered (excluding Stone weight)

7th March 2025

- Aadhaar Card

- PAN Card (Mandatory if Loan Amount > ₹ 50,000)

- Nominee Details

- Mobile No. (will be validated using OTP)

- Customer has to be present in the branch

What is a gold loan?

A gold loan is a loan obtained after pledging gold jewellery as collateral to a gold loan bank. The loan amount is calculated on the basis of the quantity and purity of gold.

Can I release a part of my gold?

Yes, you can. Once you have paid the amount based on the value of the gold, you can partly release your gold.

Where can I repay my loan amount?

You can pay your SMC gold loan through the app , or through UPI payment or visit your branch to pay the amount in cash. As a regulatory requirement we cannot accept third party payments.

How much time does it take for loan approval and what is the gold loan interest rate?

Maximum processing time to disburse SMC Gold Loan is max. 30 mins. You can get the best attractive interest rate with SMC Gold Loan based on the Gold loan scheme suitable to your requirement.

How will the value of my gold be calculated?

The value of the gold is calculated in accordance with the per gram rate in the market. Therefore, the amount will be gold loan per gram of gold jewellery to be pledged with SMC Gold Loan. While evaluating the weight of the jewellery, only the gold parts are calculated and the stones and other metals are not considered.

What is the kind of security against which I can avail the loan?

You can avail the loan against the pledge of your household ornaments. The loan offered shall depend upon the purity level of your ornaments and the net weight of gold content.

Can I avail loan against my gold bullion (coins, gold bars, gold biscuits etc)?

As per regulatory guidelines, we are not permitted to finance against the pledge of your gold bullion, bars, biscuits, coins or raw gold. For more information on the type of ornaments that can be accepted as pledged for gold loan purposes please visit your nearest branch of SMC Gold Loan

How do I know that my gold is safe with you?

Our staff follows strict operating guidelines while handling customer ornaments. This avoids ornament breakage and loss. The ornaments are kept in safe custody (safe rooms or strong rooms) with adequate security measures in the branch. There is 24 X 7 surveillance of the branch with help of our security partners.

Is there any maximum and minimum limit for availing Gold Loan? What about the tenure of the loan, lock-in period?

SMC Gold loans can be availed for any amount between Rs. 5,000/- to a maximum of Rs. 25,00,000/-. Loans can be availed for a period of min 6 months to max 12 months. Our gold loans have a minimum lock period of 7 day.

HOME

HOME APPLY ONLINE

APPLY ONLINE CONTACT US

CONTACT US CAREERS

CAREERS PAY ONLINE

PAY ONLINE GOLD LOAN PAYMENT

GOLD LOAN PAYMENT